Multifamily is its own sub-asset class

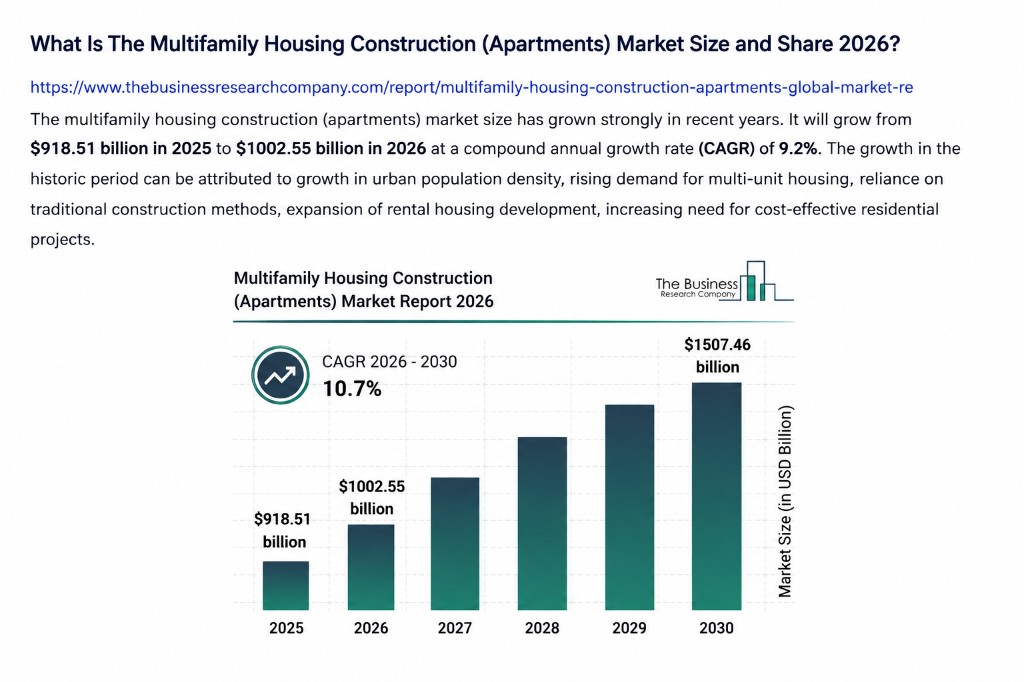

Within the broader CRE bucket, multifamily is large enough to be analyzed on its own terms. The multifamily housing construction market alone is on a long-term growth trajectory, and its capital intensity continues to support persistent demand for both construction and stabilized-asset financing.

This matters because the operating fundamentals of multifamily — household formation, renter retention, location-level supply absorption — are mechanically different from the operating fundamentals of office, industrial, retail, or hospitality. A sector that runs on tenants who sign month-to-month or annual leases reacts to rate environments very differently from a sector that runs on five- or ten-year corporate leases.

Sector dispersion is the part that actually matters

The sector-level vacancy picture is where the dispersion shows up clearly. Office vacancy is structurally elevated. Multifamily and industrial fundamentals are comparatively healthier. Retail and hospitality each run their own narrower sub-cycles within that.

CRE is not one market. It is five markets with the same accountants.

The implication for a disciplined credit underwriter is that asset-class-level theses are blunt instruments. A sector-level thesis is meaningfully sharper. A property-level thesis sharper still. The differential between average underwriting and well-underwritten exposure widens precisely when sector dispersion widens — and sector dispersion is wide right now.

Office is real, but it is not all of CRE

Office stress is the easiest CRE storyline to write about. It is also the storyline that risks anchoring readers to a single segment when the data is much wider. Office is a material component of maturing CRE debt and a real driver of headline risk, but it is one slice of the total picture.

The framing that matters: office is a sector-specific structural reset that is being absorbed slowly. Multifamily, industrial, and select retail and hospitality are running through cyclical resets that look very different at the asset level. Treating them as if they were the same exposure is the kind of analytical shortcut that produces poor outcomes in either direction — too pessimistic on the healthier sectors, too optimistic on the structurally stressed ones.

What a credit-side thesis actually looks like

For a fixed-income allocator, sector dispersion is operationalized through three filters:

- Sector selection. Which sub-cycles support durable underwriting under today's rate and demand assumptions, and which do not. Multifamily, with the supply wave cresting and the affordability gap supporting renter demand, is one of the sub-cycles that lines up.

- Lender cohort. Which lender categories sit in front of the borrower base for a given sector, and what that implies for workout pace and refinancing terms.

- Basis discipline. Where the price reset has gone the furthest, the basis-supported coupon is meaningfully more defensible than the headline coupon alone.

This is not a thesis about CRE writ large. It is a thesis about multifamily credit in a refinancing cycle, with the asset-class scale providing capital-flow support and the sector dispersion providing selectivity.

The risk of a CRE-wide narrative

The largest risk to an investor evaluating CRE exposure right now is letting the asset-class-level narrative substitute for sector-level diligence. The headlines that paint all of CRE with the same brush serve a media purpose, not an underwriting purpose. The dispersion under the headline is where the actual risk and the actual return lives.

Disciplined credit operators do the unglamorous work of staying in the part of the market where the math is defensible. The asset class is large enough, and the sector dispersion wide enough, that there is plenty of room to be selective.

Where this fits

The webinar covers this dispersion across three charts — multifamily market size, CRE vacancy by sector, and the value of U.S. commercial real estate. Continue to /fixed-income-webinar for the live briefing, or pair this with the maturity wall article for how sector dispersion expresses inside the refinancing cycle.

For the offering this thesis informs, see DF Income.

Nothing here is personalized investment, tax, or legal advice. Offerings are described in their official offering documents and are available only where lawfully offered.