Starts can bounce — the underlying trend is the story

There is a temptation to read every monthly starts release as a verdict on the cycle. It is not. Starts can jump quarter to quarter even when permits remain weak, because builders sometimes pull permits forward, defer starts, or finish what they already broke ground on. The cleaner read is the permits-to-starts relationship over time, not the headline number on any given month.

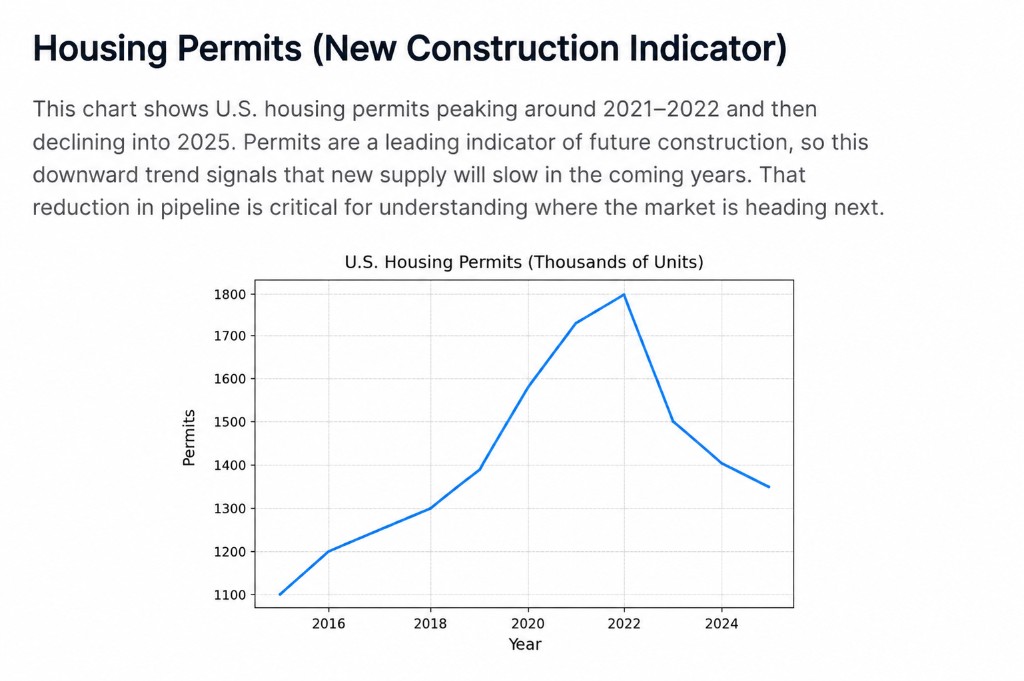

Starts make the news. Permits make the cycle.

When starts diverge upward from a softer permits trend, that gap usually closes — by starts coming down, not by permits jumping back. The forward arithmetic of construction does not let starts run ahead of permits indefinitely.

Deliveries are the part the market actually feels

Deliveries are the moment the unit hits the market and competes for a tenant. The 2023–2024 delivery wave was, in many metros, the largest in a generation. That is the wave that pressured rents in Sun Belt cities, lifted concessions, and pushed vacancy higher in pockets.

What changes from here is not demand collapsing — it is supply normalizing. The pipeline filling that 2023–2024 wave was financed at very different rates than what is available today. The next two years' worth of deliveries was permitted when capital was cheaper and underwriting was looser. As that vintage rolls off, what gets delivered after declines materially.

Multifamily starts told the same story earlier

Look at multifamily starts in isolation and the shape is even sharper. Starts surged in the low-rate window and peaked shortly after 2021. They have declined since as financing costs rose, equity capital tightened, and basis became less forgiving. Developers are pulling back. They are not pulling back because the long-term demand picture changed — they are pulling back because the math does not work at today's cost of capital for the merchant-build model.

That is exactly the kind of supply discipline that resets the next cycle's pricing power back toward the existing stock.

What this means for fixed-income capital

If the supply wave is cresting and the forward pipeline is thinner, three things become more durable:

- Occupancy. Existing well-located inventory faces less direct competition over time.

- Rent stability. Pricing power gradually shifts back from the new-supply asset toward the in-place asset.

- Income coverage. Debt service coverage on stabilized assets benefits from improved net operating income trajectories.

None of this is a v-shaped recovery story. The 2023–2024 wave still has to fully absorb. Vacancy normalization is gradual. But the direction of the leading indicators has changed, and that matters for how a disciplined lender underwrites the next eighteen to thirty-six months.

Where this fits

The webinar walks through this evidence across six charts — permits, starts, deliveries, supply waves, the recovery timeline — and ties them to where private fixed-income capital is positioned to underwrite. Continue to the live briefing on /fixed-income-webinar for the full deck, or read the companion piece on the maturity wall for the debt-side picture.

For the offering this thesis informs, see DF Income.

Nothing here is personalized investment, tax, or legal advice. Offerings are described in their official offering documents and are available only where lawfully offered.