What that gap actually does to renter behavior

Two things follow directly:

- Renters stay renters longer. The household that would have transitioned to ownership in a more normal market is no longer making the math work, so it stays in the rental pool.

- Move-outs to ownership decline as a churn driver. That is the cleanest way the affordability gap shows up in an operator's data: lower turnover, longer renewals, more pricing power on the renewal trade than on the new-lease trade.

Neither effect requires a thesis about rent growth in absolute terms. They just require fewer renters being pulled out of the rental pool, which is exactly what the affordability gap produces.

When ownership stops penciling, renters stop being temporary.

This is a quieter dynamic than the headlines around home prices or mortgage rates, but it is the one that shows up first in operating data.

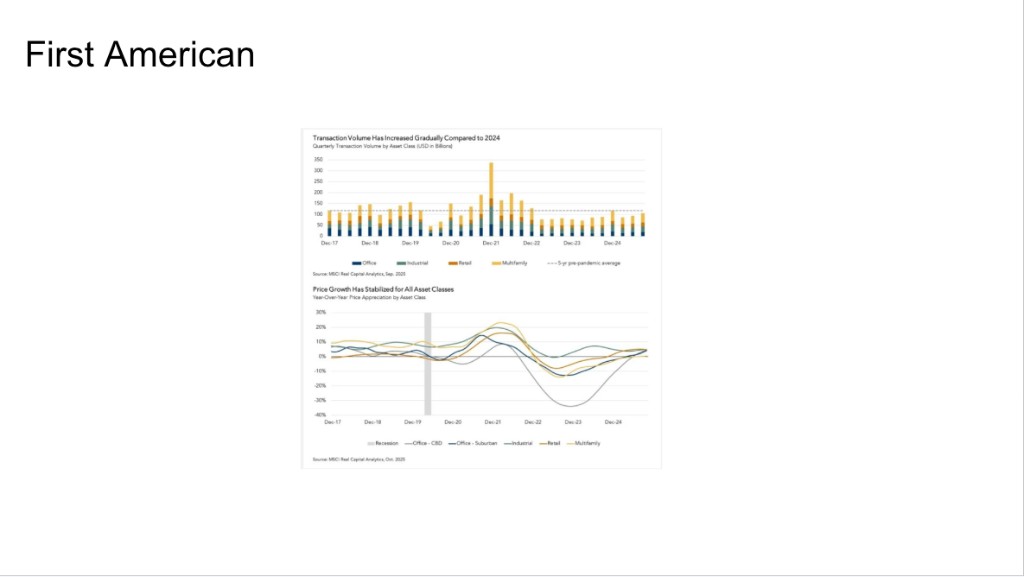

The forecast keeps the gap open

CBRE's projection of average monthly multifamily rent versus a new home mortgage payment shows the gap persisting — and in some metros, widening — over a multi-year window. The drivers underneath the forecast are not exotic: mortgage rates are not expected to fall back to early-cycle levels on a sustained basis, home prices have held more firmly than skeptics expected, and the cost-of-ownership math therefore continues to favor renting across many high-population metros.

This is not a forecast about rent acceleration. It is a forecast about renter retention, which is a different and more durable input to operating fundamentals.

What this means for credit underwriting

For a fixed-income allocation against multifamily collateral, the affordability gap matters in three specific places:

- Occupancy assumptions. A renter pool that is being topped up rather than drained supports more conservative occupancy underwriting.

- Renewal economics. Renewals tend to outperform new leases in pricing power when the alternative-housing math is unfavorable. That stabilizes net operating income.

- Downside scenarios. In a soft macro environment, the affordability gap acts as a cushion — renters cannot easily exit to ownership even when discretionary budgets tighten.

None of this is a substitute for asset-level diligence. But it is a tailwind that runs underneath the underwriting and gets stronger, not weaker, when broader uncertainty rises.

Where the dynamic is strongest

The affordability gap is wider in metros where home-price levels are highest relative to incomes — coastal and high-cost markets in particular — but it is now meaningful across most major metros. Sun Belt cities, which absorbed the bulk of the 2023–2024 delivery wave and where prices moved fastest, have seen the gap widen even where rent growth has been softest.

That dispersion is again the useful part of the picture. The metros where deliveries pressured rent the most are often the same metros where the affordability gap is now actively pulling renters back into the rental pool. The two forces work in opposite directions, which is why the supply wave is cresting without producing a full-cycle rent collapse.

What the affordability gap is not

It is not a call that home prices are about to break. It is not a call that mortgage rates are about to drop. It is not a call on home ownership policy. It is a structural observation that, given current rates and current home prices, the monthly arithmetic favors renting in most major metros, and that arithmetic is already in renters' decisions today.

For a long-duration, income-oriented allocation, that arithmetic is one of the more durable inputs available right now.

Where this fits

The webinar covers this dynamic across two charts — the rent-vs-mortgage multiplier and the projected gap over the forecast horizon. Continue to /fixed-income-webinar for the live briefing, or pair this with the supply-wave article for the cause-side picture and the where-rents-go article for the rent-stabilization view.

For the offering this thesis informs, see DF Income.

Nothing here is personalized investment, tax, or legal advice. Offerings are described in their official offering documents and are available only where lawfully offered.