There is no fourth option. The rate environment does not let borrowers wait out the gap indefinitely.

What DSCR compression actually does

Debt-service coverage ratio is the ratio of net operating income to debt service. When rates rise and DSCR falls, every covenant in a typical CRE loan document starts to apply differently. Cash sweeps trigger earlier. Reserve requirements kick in. Springing recourse provisions become live.

The borrower does not have to default for any of this to matter. The borrower just has to operate inside the new constraint, which usually means less optionality, less time, and more pressure to act before the next rate decision.

A rate gap is not a coincidence. It is a forcing function.

For a disciplined credit underwriter, the value of this dynamic is not in chasing distress — it is in being the counterparty of choice when a borrower needs to act on terms that are still defensible on both sides.

The credit spread: wider risk pricing on top of Treasuries

The rate gap is not only about Treasury yields. CRE mortgage spreads over Treasuries have widened versus pre-cycle averages. Lenders are pricing risk more carefully and demanding more for the same exposure. That is normal in a repricing cycle.

For lenders, spread expansion is a tailwind on well-underwritten deals — it improves the return on capital for taking the same fundamental risk. For borrowers, it compounds the rate gap, because the gap is rate + spread, not rate alone.

The shape of the spread curve also matters. When spreads are wide, the cost of getting capital for a marginal deal can become prohibitive, which itself filters the deal flow that actually closes. The deals that get done in this environment are, by selection, the deals that can carry the math.

The price reset: a lower basis underneath the new coupon

Cumulative CRE price changes since the cycle peak show that the repricing process has already occurred in many pockets. Transaction-based marks and appraisal-based marks tell slightly different stories, but the direction is the same: basis has moved.

That movement is what makes the higher coupon underwriteable. A loan originated against a lower basis carries different risk than the same coupon written against peak pricing. The math is straightforward:

- Lower basis = lower leverage at the same loan dollars

- Lower leverage = more cushion in the cash flows

- More cushion = a defensible coupon, not just a high coupon

This is the part of the cycle that disciplined credit teams spend the most time on. The coupon does not exist in isolation — it sits on top of a basis that either supports it or does not.

Stabilization signals after the repricing

Recent transaction and pricing data from major market datasets — including First American's snapshot — suggest stabilization is emerging after the repricing phase. Activity remains uneven by segment. But the pattern is the one that typically marks the early stage of a new deployment cycle: prices stabilize, transaction volume gradually returns, and bid-ask spreads narrow.

This is not a signal to rush. It is a signal that the documentation work done now — on offerings underwritten to today's data — is more valuable than the documentation work done a year ago against an environment that was still moving.

What this means for income-oriented allocation

Three threads of the math come together for a fixed-income allocator:

- Coupon defensibility. Coupons earned in this environment are earned against wider spreads, lower basis, and more conservative LTVs — provided the underwriting reflects those inputs.

- Covenant strength. Lenders writing into rate-pressured borrowers have leverage on structure that lenders did not have a vintage ago.

- Deal selection. The opportunity is not "average CRE credit." It is the subset of situations where the rate gap, the spread, and the basis reset all align for the lender.

The cycle does not reward the loudest coupon. It rewards the most clearly underwritten one.

Where this fits

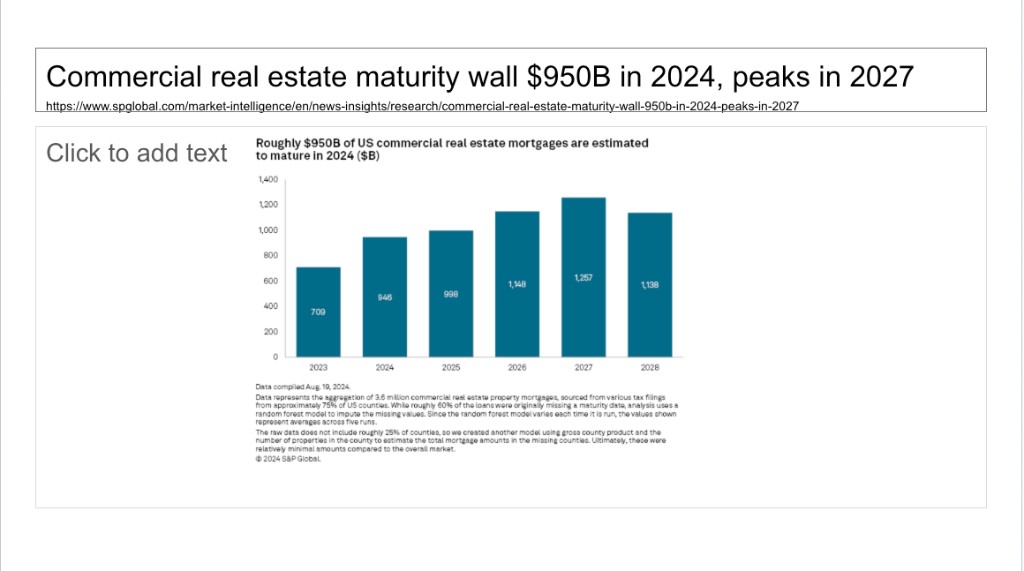

The webinar covers this ground across four charts — the refinancing rate gap, CRE mortgage spreads vs Treasuries, the cumulative price change, and the First American snapshot. Continue to /fixed-income-webinar for the live briefing, or pair this with the maturity wall article for the size and tempo of the refinancing cohort.

For the offering this thesis informs, see DF Income.

Nothing here is personalized investment, tax, or legal advice. Offerings are described in their official offering documents and are available only where lawfully offered.